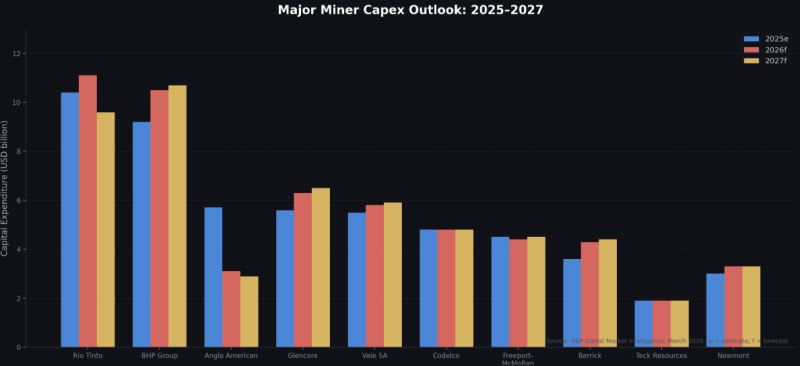

The top 30 miners are projected to spend $121.6 billion in 2026, a decade high.

After the supercycle bust of 2013–14, the sector spent a decade deleveraging. Free cash flow went to balance sheets, not projects. Now capital is moving again, but the character of that spending tells a different story to the headline number.

Copper dominates the agenda with BHP, Rio Tinto, Glencore and Freeport-McMoRan all flag it as the priority. But look at where the money is actually going. Brownfield expansions. Debottlenecking. Sustaining capex at mature operations.

Resolution, El Pachón, Sakatti are either deferred or still years from first production. Anglo American is cutting capex to the bone ahead of a potential Teck Resources Limited merger. Vale trimmed its 2025 budget by $1 billion.

The industry is spending more, but it's spending defensively. Cash-generative incumbents are being sweated harder. New supply isn't being built, it's being studied, postponed, or quietly shelved.

This matters because the demand projections driving these investment decisions assume copper, nickel and critical minerals will be needed at scale within the decade.

The supply response required to meet that demand isn't in the pipeline at the pace or volume needed. Capex is rising, but the structural gap between what's being built and what will be needed keeps widening.

After 2027, spending is forecast to fall again as major projects wind down. The industry will face the same growth dilemma it's been circling for years just with less time to solve it.

Rational decisions at the company level. A collective failure at the industry level.

For more of my takes on the resource industry sign up to my weekly newsletter www.kamoacap.com

Source: S&P Global Market Intelligence, March 2026

Mining operations depend heavily on a reliable and well-coordinated logistics and purchasing system. From the procurement of heavy machinery to the timely delivery of spare parts, explosives, and fuel, logistics serves as the invisible backbone of mine productivity. Effective purchasing and supply chain strategies not only minimize operational delays but also ensure that mining projects remain economically viable and environmentally responsible.

1. The Strategic Role of Logistics in Mining

Mining logistics involves the planning, movement, and storage of materials throughout the value chain from exploration sites to processing plants and export terminals. Given the remote locations of many mines, logistics must address challenges like poor infrastructure, unpredictable terrain, and long transport routes.

To overcome these, companies are increasingly turning to integrated supply chain systems, satellite tracking, and route optimization software. These tools enhance real-time visibility, reduce transportation costs, and minimize fuel consumption, contributing to more sustainable operations.

2. Purchasing as a Cost-Control Mechanism

Purchasing is more than procurement it is a strategic cost-control process. Through centralized purchasing systems, companies can negotiate better supplier contracts, improve inventory accuracy, and reduce duplication of materials. In modern mines, digital procurement platforms allow engineers and procurement officers to monitor stock levels, approve purchases online, and prevent unnecessary expenditure.

Strategic sourcing also encourages partnerships with local suppliers, supporting regional economies and strengthening community relations a vital part of corporate social responsibility in mining.

3. Technology and Automation in Logistics and Purchasing

The integration of automation and digital tools has transformed mining logistics. Technologies such as blockchain, RFID tagging, and automated inventory systems have enhanced transparency and traceability across the supply chain.

Blockchain, for instance, allows mining companies to verify the ethical sourcing of materials, ensuring compliance with global standards such as the OECD Due Diligence Guidance. Meanwhile, predictive analytics tools can forecast demand for consumables or parts, reducing downtime and optimizing warehouse management.

4. Sustainability and Environmental Considerations

Logistics and purchasing decisions significantly influence a mine’s environmental footprint. Optimized haulage routes reduce emissions, while eco-friendly packaging and material recycling contribute to sustainable practices. Responsible procurement policies that prioritize suppliers adhering to environmental and ethical standards further strengthen a mine’s commitment to sustainability.

5. Challenges and Future Perspectives

Despite digital progress, mining logistics still faces hurdles like fluctuating fuel prices, global supply chain disruptions, and geopolitical risks. To navigate these, companies must adopt resilient supply chain models and diversify sourcing channels.

Looking forward, the integration of artificial intelligence (AI) and green logistics technologies — such as electric haulage trucks and renewable-powered supply networks will redefine how mines manage resources and deliver materials efficiently.

Source: https://en.wikipedia.org/wiki/Supply_chain_management%20Additional%20References:%20•Deloitte%20(2023).%20Digital%20Supply%20Chains%20in%20the%20Mining%20Sector.%20•McKinsey%20&%20Company%20(2022).%20Building%20Resilient%20Mining%20Supply%20Chains.

Don’t just track savings if you want top procurement

I’d do this instead...

Track metrics that align with your business goals.

Group the KPIs for better decision-making:

➝ Quality KPIs – To assess supplier performance.

➡️ Compliance rate, Supplier defect rate, Purchase order accuracy

➝ Inventory KPIs – To assess effective order management

➡️ Inventory turnover ratio, Inventory carrying cost, Inventory aging

➝ Cost-Saving KPIs – Evaluate procurement's level of impact

➡️ Cost avoidance, Procurement ROI, Spend under management, Cost reduction

➝ Delivery KPIs – To assess a reliable supply chain

➡️ Vendor availability, Purchase order cycle time, Supplier lead times

Most Procurement teams only track two or three of these metrics and then struggle to improve YOY or even to justify their value

The first 90 days are critical for any CPO, Head or Senior Procurement manager to make an impact

(It's also the most commonly asked interview question)

I've created this cheat sheet for you. 🎁

The part most people miss in planning for the first 90 days is the importance of splitting into three distinct sections:

30 days: Understand the Business

60 days: Understand the spend landscape

90 days: Deliver an aligned vision

The way you do this should be broken down further.

The first 30 days

- Engage Stakeholders

- Establish Requirements

- Understand the Business

- Learn through internal review

Days 30 to 60

- Meet key suppliers

- Understand the spend

- Learn through External Review

- Understand the change opportunity

Days 60 to 90

- Align your plan with the business

- Deliver a roadmap for success

- Create a vision to achieve

- Drive a dynamic Procurement plan

The end point of this first 90 days has to be an exec sign off session to ensure

a.) alignment to the strategy and

b.) full top down endorsement

If you don't have a plan like this for the first 90 days, you're unlikely to deliver strategic impact in a business.

It's the very difference between taking on a tactical Procurement role versus a leadership role.

Many struggle to make that step up because they don't have a plan for the delivering impact

And because they misunderstand the importance of building the foundations.

In the cheat sheet below, I've also included the key tasks that need to be delivered in 30/60 and 90 days.

A checklist if you like.

Has this helped?

____________________

📌 Do you want a hi-res PDF of this cheat sheet and all the other ones I release straight to your inbox?

I’m Tom Mills Procurement Protagonist®️

I simplify Procucurement.

Simply sign up to my free newsletter here:

https://procurebites.com/

You’ll get this cheat sheet and other valuable gems for free, released every Monday via the newsletter.

The request for information (RFI) or request for quotation (RFQ) process is an essential part of procurement management in order to make informed decisions about potential suppliers. An RFI is used to gather information about potential suppliers and their capabilities, while an RFQ is a concrete request for quotation (a solution proposal and a price).

The first step of the RFI is to identify the company's internal requirements. This includes clarifying the required information, such as specific characteristics, quantities and delivery times. An RFI document is then created that clearly defines the background, specific questions and desired response formats. This is followed by the selection of potential suppliers who are able to provide the required products or services. The RFI is sent to the selected suppliers, who then submit their responses. These are carefully analysed to assess suitability and potential for future collaboration. If necessary, further questions are asked or additional information obtained. Based on the responses received, a shortlist is drawn up with the most relevant suppliers who are eligible for further steps. The suppliers are informed of the result of the RFI and receive feedback or an invitation to the next phase.

In the case of an RFQ, the company specifies its requirements and documents in detail the desired goods or services, the conditions, delivery deadlines and evaluation criteria for the selection of offers. The RFQ document is then sent to the previously identified potential suppliers, who are invited to submit a quotation. The bids received are evaluated based on the specified criteria. The supplier that best fulfils the requirements is then selected. If necessary, contract terms, prices or delivery details are negotiated. After the final selection, the contract is awarded to the supplier, formalising the business relationship. Finally, an official purchase order or contract is drawn up, setting out all the relevant terms and conditions. This structured and transparent process enables companies to make informed decisions, minimise risks and ensure efficient collaboration with suppliers.

https://www.linkedin.com/in/mariobuesch/

The world’s top 20 mining OEMs generated over $66 billion in mining and metals sales in 2024 — but with geopolitical uncertainty, shifting commodity demand, and the slow roll of electrification, the future looks anything but predictable.

From Komatsu, Caterpillar Inc. and Epiroc to rising Chinese players like SANY Group and XCMG Group these companies are facing the biggest industry reset in history — and the race to electrification is on.

While Sandvik and Liebherr Group are making strides in battery-electric tech, even leaders like Metso and Hitachi CM admit tariff turbulence and global decoupling could reshape market activity.

📉 With copper demand expected to rise 70% by 2050, but new projects facing delays, OEMs will play a pivotal role in keeping the supply chain moving.

View the full article in the comments. A must-read for anyone watching where mining equipment, innovation, and strategy are headed next.

Source: Credit to International Mining and Resources Conference (IMARC)

When procurement is done right, it leads to:

✅ Smarter spending

✅ Stronger supplier relationships

✅ Seamless operations

✅ Better results

But often, inefficiencies creep in:

❌ Delayed approvals

❌ Missed cost-saving opportunities

❌ Supplier conflicts

❌ Repeated errors

Here’s how to master procurement:

1️⃣ Need Identification

Understand what your organization needs and define clear specifications.

KPIs: Percentage of accurately identified needs, number of specification revisions.

2️⃣ Purchase Requisition

Formalize internal requests and streamline approvals.

KPIs: Requisition approval cycle time, percentage of requisitions approved without revisions.

3️⃣ Supplier Identification

Research and shortlist suppliers based on capacity, reliability, and quality.

KPIs: Number of qualified suppliers identified, supplier qualification lead time.

Etc

Website: https://stan.store/Kingslys/p/cargocheatsheets-membership

The preparation and successful execution of negotiations is one of the key competences in procurement. This overview contains some of the central elements for developing this competence.

1️⃣ Every expert in negotiations once started with none. The integrated procurement competency model defines three levels for each competency area, starting with Advanced Beginner, Competent and Expert.

2️⃣ Negotiation is not an event, but a process. In addition to the preparation, execution and follow-up of a negotiation, there are also two phases for the annual, overarching planning of negotiations.

3️⃣ The following overview deals with negotiation tactics. Roughly speaking, the possible tactics can be divided into five groups: delay, collaboration, manipulation, power and pressure.

4️⃣ The right preparation for a negotiation is one of the success factors. There are 9 main areas to consider: (I) negotiating team, objectives and timetable; (II) power analysis; (III) BATNA and alternatives; (IV) facts and interests; (V) negotiation strategy; (VI) possible options; (VII) negotiation tactics; (VIII) compromises and concessions; and (IX) opening of negotiations.

5️⃣ In the centre is a form with the 9 areas described above. It is important to be clear about your own position as well as the possible position of the other party (the supplier).

6️⃣ In team negotiations, it is important to be clear about the different roles in a negotiating team and to prepare accordingly.

7️⃣ A negotiation always involves interaction between the negotiating parties. Where there is interaction, there can also be conflict. It is important to know your own preferences and the preferences of your own team members.

8️⃣ Your own preference does not always have to coincide with the strategy defined before the negotiation: (I) AVOID - procrastinate to win; (II) ADAPT - lose to win; (III) COMPETITION - win/lose; (IV) COOPERATE - win/win; and COMPROMISE - splitting the difference.

9️⃣ Finally, an overview of active listening with its 5 steps: encourage, clarify, circumscription, reflection, and confirmation.

Dr. Mario Büsch, Purchnet

https://www.linkedin.com/in/mariobuesch

A team of researchers from Fraunhofer FFB and the German University of Münster has analysed the ownership structures and geopolitical dependencies along the supply chain for electric car batteries. The results of the study show that China is clearly in the lead when it comes to securing raw materials.

The analysts conclude that the People’s Republic of China controls almost the entire value chain from the extraction of raw materials to the production of batteries – and controls domestic production facilities, as well as those abroad. Of the four raw materials analysed – lithium, nickel, cobalt and manganese – only manganese is an exception. The refinement of the raw materials and the construction of the actual cells and batteries is also dominated by China, as the latest annual analysis by SNE Research shows. The leading duo CATL and BYD alone account for 55 per cent of the global market share for installed battery capacity in electric cars.

As the Fraunhofer FFB explains, large battery packs, such as those installed in a Tesla Model S Plaid, contain around 122 kilograms of so-called mineral raw materials. Geographically, only a few countries have the resources needed in large quantities for the expansion of electric mobility. These include China, Australia and the Democratic Republic of the Congo. The challenge: “Mineral raw materials are at the very beginning of the supply chain for battery cell production, and Europe is almost 100 per cent dependent on imports,” says Professor Simon Lux, Director of Fraunhofer FFB.

=> Securing raw materials in Europe and the USA: between catching up and dependency

In Lux’s view, China’s growing dominance of raw materials jeopardises the future of European electric mobility: “This dependency makes Europe vulnerable. Geopolitical tensions or export stops could lead to massive economic damage and losses running into billions.” Although Europe and the US are intensifying their efforts to gain greater control over the supply chain for lithium-ion batteries by acquiring mines and refineries, Europe’s share has so far been comparatively small. The US is making better progress – at least as far as lithium is concerned.

According to the authors of the study, Australia, Indonesia and the Democratic Republic of the Congo – all key regions for mining lithium, nickel and cobalt – are particularly affected by company takeovers. For example, 74 per cent of the world’s lithium comes from Australia and Chile, but Chinese (29 per cent) and US companies (26 per cent) hold the largest shares of production. “These developments underline the global competition for critical raw materials and the strategic realignment of value chains,” says Lux.

For the four raw materials analysed – lithium, nickel, cobalt and manganese – the study outlines the following picture of global ownership and influence:

Lithium: 74 per cent of the world’s lithium comes from Australia and Chile. Nevertheless, companies such as Tianqi Lithium from China and Albemarle from the USA hold the largest shares of global production, with China accounting for 29 per cent and the US for 26 per cent. Europe has almost no lithium shares abroad. Europe’s own shares are negligible and have so far been limited to the Baroso lithium project in Portugal, which accounts for just 0.4 per cent of production.

Nickel: Although 30 per cent of global nickel production takes place in Indonesia, Indonesian companies account for less than five per cent of production. Chinese companies, such as Tsingshan, secure 86 per cent of the remaining production in Indonesia, meaning China has the greatest control (32 per cent) over nickel production in combination with domestic production. The most influential regions after China include Europe, the Philippines and Russia, which together account for just over 40 per cent of global production.

Cobalt: Local companies control only five per cent of the mines, although 68 per cent of global production takes place in the DR Congo. China (47 per cent) and Europe (47 per cent) dominate production there – with players such as CMOC, Glencore and Eurasian Resources Group (ERG). Outside Chinese and European control, the Philippines, Russia and Cuba are influential (12 per cent).

Manganese: Australia is expanding its influence to a total of 25 per cent by acquiring more than half of South African mining rights through the companies South 32 and Jupiter Mines. South Africa is in second place with 20 per cent, followed by Europe, which has a total share of 16 per cent of global manganese production. These shares are spread across mines in Australia, Gabon and Ukraine, which were acquired by Anglo American, Eramet and ERG.

The analysts note that China has a particularly large lead in the LFP battery sector. Accordingly, China produces the majority of lithium iron phosphate active materials with a share of more than 98 per cent. The conclusion is that this means Europe is directly dependent on this more cost-effective battery chemistry. So, what can be done from a European perspective? According to the authors, possible levers for a secure and sovereign battery supply chain in Europe could be investments in expanding Europe’s own refinery capacities, promoting strategic raw material partnerships and strengthening the local circular economy.

In terms of methodology, the researchers from Fraunhofer FFB and the University of Münster state that the study is based on a comprehensive data analysis. To this end, the ownership structures along the global lithium-ion battery supply chain were analysed and compared with the geographical distribution of production shares. The study’s initiators aimed to “draw a holistic picture of the current power structures in the industry.”

Source: https://www.electrive.com/2025/02/19/fraunhofer-study-measures-chinas-dominance-in-the-battery-supply-chain/#

Source: Credit to Carla Westerheide, Electrive

22 Logistics and purchasing

Focuses on supply chain, procurement, transport, and inventory management.

Logistics and procurement workshops.

No events scheduled

22 Logistics and purchasing

Focuses on supply chain, procurement, transport, and inventory management.