$121 billion in mining capex and the industry still can't solve its own supply problem

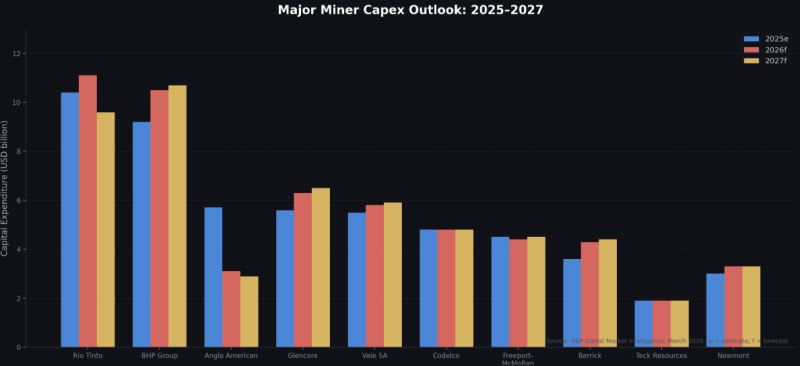

The top 30 miners are projected to spend $121.6 billion in 2026, a decade high. After the supercycle bust of 2013–14, the sector spent a decade deleveraging. Free cash flow went to balance sheets, not projects. Now capital is moving again, but the character of that spending tells a different story to the headline number. Copper dominates the agenda with BHP, Rio Tinto, Glencore and Freeport-McMoRan all flag it as the priority. But look at where the money is actually going. Brownfield expansions. Debottlenecking. Sustaining capex at mature operations. Resolution, El Pachón, Sakatti are either deferred or still years from first production. Anglo American is cutting capex to the bone ahead of a potential Teck Resources Limited merger. Vale trimmed its 2025 budget by $1 billion. The industry is spending more, but it's spending defensively. Cash-generative incumbents are being sweated harder. New supply isn't being built, it's being studied, postponed, or quietly shelved. This matters because the demand projections driving these investment decisions assume copper, nickel and critical minerals will be needed at scale within the decade. The supply response required to meet that demand isn't in the pipeline at the pace or volume needed. Capex is rising, but the structural gap between what's being built and what will be needed keeps widening. After 2027, spending is forecast to fall again as major projects wind down. The industry will face the same growth dilemma it's been circling for years just with less time to solve it. Rational decisions at the company level. A collective failure at the industry level. For more of my takes on the resource industry sign up to my weekly newsletter www.kamoacap.com Source: S&P Global Market Intelligence, March 2026