- Z-POSTS (4)

- Z-NOTES

- Z-EVENTS

- DESCRIPTION

- Item 1

13 Reserve calculations

Add Z-POSTZ-POSTS is a public space. The content written here will be visible to the ZVENIA community.

ZVENIA Mining .13/05/2024

ZVENIA Mining .13/05/2024Why is this Issue so Important?

The metal price(s) are one of the most significant sources of uncertainty in mine project evaluation – this is because any variation from the expected metal price may considerably modify the results of the entire project value and, consequently, mislead strategic operational and economic decisions, investment decisions and even lead to erroneous conclusions of and for impairment decisions.

The Problem

Writing for the International Journal of the Central Bank, March 2018, Jorge Fornero and Markus Kirchner had this to say in their article entitled: Learning about Commodity Cycles and Saving Investment Dynamics in a Commodity-Exporting Economy: “…the evolution of copper price forecasts by professional forecasters of the CRU Group (reports in October of each year), as shown in figure 4. The rise of the spot price in the mid-2000s was not validated by higher forecasted prices on a medium to long-term horizon.

Instead, it was considered as a transitory price increase by the professional forecasters who predicted that the spot price would return to values of around 100 cents. Due to the crisis, the price fell and almost reversed the rise from 2003 to 2007, reaching a minimum of approximately 140 cents (where the annual average understates somewhat the dynamic evolution of the spot price). That decline was relatively short-lived, and after the crisis the copper price quickly recovered and exceeded its pre-crisis levels. However, the higher post-crisis prices were also accompanied by higher forecasted prices, as part of a process of gradual forecast revisions that had already started around 2007. In the following years, the forecasted prices reached values much closer to the effective spot price. Hence, the professional forecasters seem to have incorporated a more persistent price increase in their forecasts over time. More recently, as the commodity cycle has turned and prices have fallen, it has taken the forecasters again several years to adjust their expectations on future prices downwards.”

It would be unfair to single out a single forecaster as no single forecaster has got it right in the past. Bloomberg published “consensus” forecasts of the gold price in 2015. Notably the long- term “consensus” forecast in 2012 was USD/oz 600. Fast forward to 2015 and the “consensus” forecast was circa US/oz 1 300; that is a 100% variation. Often it is underlined that the long-term price is not a “real” price and has to be discounted back to the year current years.

Assuming that the last price on the gold forecasts above represent the long-term view at the time of each forecast, then the “real” price at 3% using a mid-term exponent is calculated. In 2007; therefore, the long-term price assumed was USD/oz of gold 467 and in 2012 USD/oz 1 353. Cynically, in 2007 one could have randomly picked a price between USD/oz 467 and USD/oz 1 353 and been in the reasonable prediction range – with the wisdom of hindsight. On August 22, 2011 gold reach an historic high of 1917.90 – well above USD/oz 1, 353. At the time of writing the price is USD/oz 1 194.80, closer to the 2011 long-term forecast. It is perhaps a fair statement that volatility plays havoc with forecasters forecasts.

So the problem is simple – one cannot with any degree of confidence rely on forecasters long-term forecasts of metal prices, and yet so much reliance is placed upon these forecasts. An even more tragic reality is that when the forecasts are averaged ad named “Consensus” they assume an even greater weighting. It is safe to say that the average of wrong remains wrong.

Perhaps Warren Buffets comment that ” Forecasts tell you a great deal about the forecaster; they tell you nothing about the future,” has some substance. One thing is clear; forecasters forecasts are always wrong and yet the industry places significant confidence on the collective opinion despite the collective forecast that in addition to being wrong is also insanely fluid. Perhaps it is time to seriously debate alternatives to the application of long-term price forecasts especially when it relates to the declaration of Mineral Reserves and Ore Reserves and the determination of impairment indicators.

All credits to Craig Hutton ZVENIA Mining .29/04/2024

ZVENIA Mining .29/04/2024Hoy quiero compartir con ustedes un pequeño aprendizaje del gran mundo que es la planificación minera y las herramientas de los programas para la mencionada actividad💡🌐

En esta ocasión escribí este pequeño manual con pasos breves para que los jóvenes estudiantes como yo puedan tener una guía de los temas que están en la presentación, aquí se han empleado diversas herramientas del software Mineplan para definir un modelo de bloques, puesto que este es la base para comenzar con el proceso de planificación.

Sin más que decir, espero este pequeño aporte les sea útil y espero seguir compartiendo con ustedes más herramientas de este lindo programa.🤓✨✨Credits to PAOLA LIZBETH RIVAS FLORES ZVENIA Mining .28/03/2024

ZVENIA Mining .28/03/2024La teneur de coupure (COG) est généralement définie comme “la quantité minimale de produit métallique de valeur qu’une tonne métrique de matériau doit contenir avant d’être envoyée à l’usine de traitement” ou comme “une limite artificielle délimitant la minéralisation à faible teneur et le minerai techniquement et économiquement viable qui peut être exploité avec profit”.

Par conséquent, les teneurs de coupure sont utilisées pour sélectionner les blocs de minerai des blocs de déchets à différents stades de l’évolution de l’estimation des ressources/réserves minérales d’un gisement minéral (par exemple, au cours des phases de prospection et d’exploitation).

Si la concentration de matière dans la minéralisation est supérieure à la teneur limite, elle est définie comme du minerai ; inversement, si la concentration de matière est inférieure à la teneur limite, elle est considérée comme un déchet.

Toutefois, des méthodes de mélange (minéralisation à faible teneur et à haute teneur) sont couramment utilisées dans les mines pour une utilisation efficace des ressources minérales.

Annel a classé les nombreux facteurs qui influencent la teneur de coupure en trois catégories :

1***Géologique par exemple, la minéralogie, la taille des grains, la présence d’éléments nocifs, la forme et la taille du gisement, la complexité structurelle ou les problèmes d’eau.

2***Économique par exemple, l’accessibilité aux marchés, la disponibilité de la main-d’œuvre, les conditions actuelles d’exploitation et les prix actuels des métaux, les facteurs politiques et fiscaux, le coût de l’élimination des déchets et de la remise en état, ou les coûts d’investissement et les taux d’intérêt.

3***Méthodes d’exploitation minière par exemple (mines à ciel ouvert ou souterraines) , la modification d’un seul critère ou la combinaison de plusieurs d’entre eux entraîne une modification de la teneur limite et de la teneur moyenne du gisement.

Une teneur de coupure élevée peut être utilisée pour augmenter la rentabilité à court terme et la valeur actuelle nette d’un projet minier, mais l’augmentation de la teneur de coupure est également susceptible de réduire la durée de vie d’une mine.

Cette durée de vie plus courte peut également avoir des effets socio-économiques plus importants, avec une diminution du nombre d’emplois à long terme et une baisse de la valeur de la mine ,des bénéfices aux employés et aux communautés locales.

Bien que la planification de la production à long terme d’une exploitation minière à ciel ouvert dépende de plusieurs facteurs, la teneur de coupure est probablement l’aspect le plus important, car elle fournit une base pour la détermination de la quantité de minerai et de déchets au cours d’une période donnée .

Source: Alpha Bayo

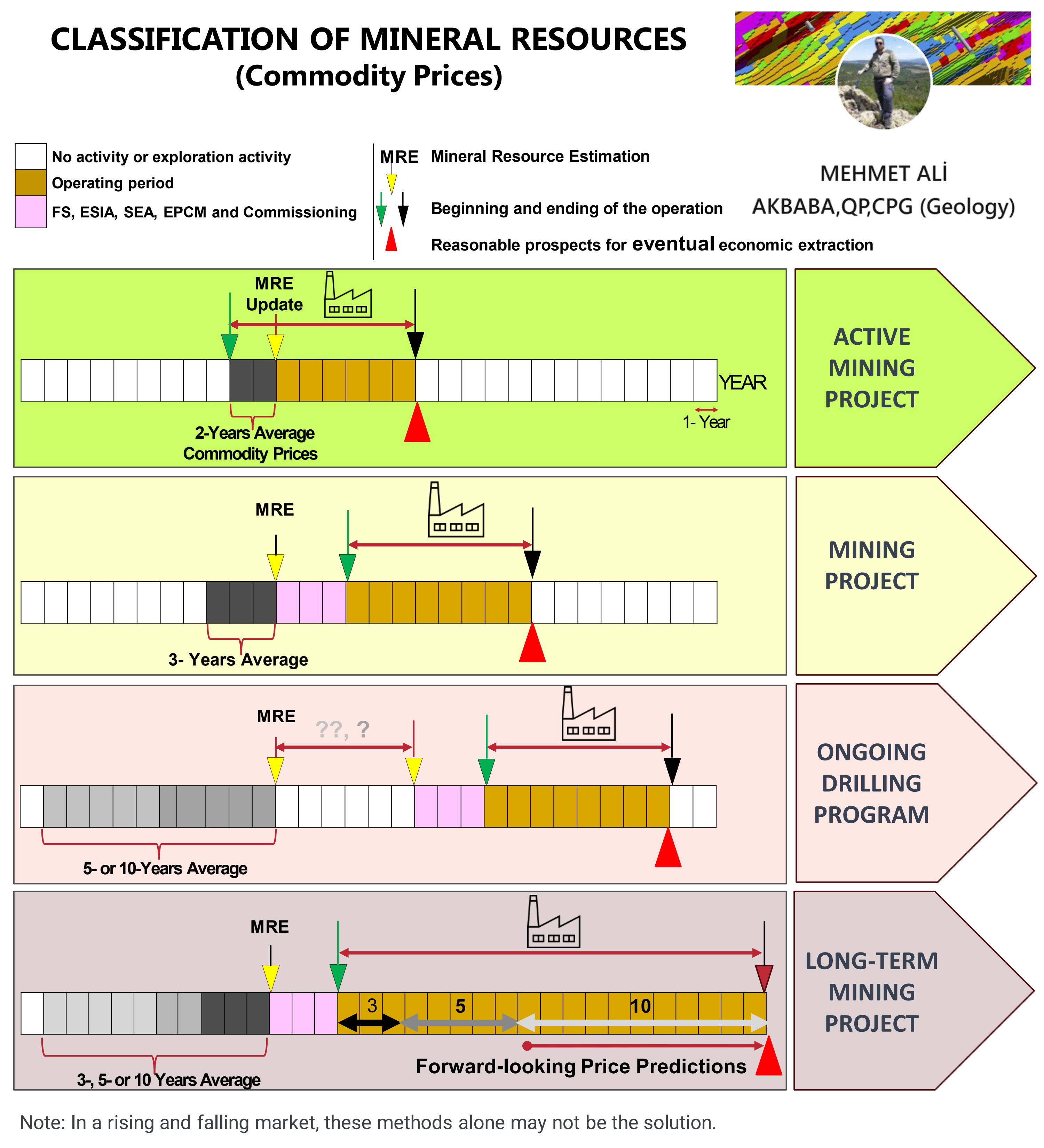

Credits to Mineral Resource (From Exploration to Sustainability Assessment)ZVENIA Mining .15/10/2023🔎Introduction

Predictions of mineral resources and reserves play a crucial role in the mining industry. These forecasts rely on economic factors, such as commodity prices, to assess the future economic extractability potential of mining sites.🔎Justification

Reasonable prospects for eventual economic extraction🔎The Role of Commodity Prices

❶ Commodity prices are a fundamental parameter in the evaluation of mineral resources and reserves.

❷ Commodity prices should be selected by a Qualified Person (QP) and clearly outlined in the technical report.

❸ Fluctuating commodity prices can impact the accuracy of predictions, necessitating careful selection by the QP.

❹ The timing of a mining site’s entry into production can affect commodity prices, thus the QP should consider long-term or short-term prices.🔎Long-Term and Short-Term Prices

① Long-term prices are supported by historical data and can be used in mineral resource predictions.

② Long-term prices do not account for annual price fluctuations, requiring meticulous analysis.

③ Short-term prices often include average prices and better reflect market fluctuations.

④ Three-year backward average prices can mitigate market fluctuations but may lead to errors in rising or falling markets.🔎Methodology Explanations

❶ The QP should elucidate the details and rationale behind the chosen prices and forecasting methods.

❷ Historical prices should be clearly indicated as to whether they are adjusted for inflation (expressed in constant dollars) or not.🔎Conclusion

Commodity prices play a significant role in predicting mineral resources and reserves. The QP must adopt a cautious and logical approach in selecting these prices, and these selections should be transparently explained in the technical report↑

#mining #geology #CommodityPrices #MetalPrices #QP #CIM #MineralResource #MineralReserve #MiningIndustry֎Reference:

① 2020 CIM Guidance on Commodity Pricing and Other Issues related to Mineral Resource and Mineral Reserve Estimation and Reporting

② Metal prices are taken from www.kitco.comSource: MEHMET ALİ AKBABA, LinkedIn

✍Valued members of the Resource Geologist group✍

- Item 2

13 Reserve calculations

Add Z-NOTEZ-NOTES is a private space. The content written here will be visible only to you.

- Item 2

13 Reserve calculations

Add Z-EVENTZ-EVENTS is a public space. Events posted here will be visible to the ZVENIA community.

- Item 2

13 Reserve calculations

In this module you will have access to the following topics (not exhaustive) :